Mixed signals for aviation: today’s carbon pricing is setting the wrong flight path to Net Zero

Comment by Emily Ford, Senior Energy Policy Advisor – Carbon Policy

Carbon pricing helps businesses to understand the cost of their emissions and make commercially informed choices about reducing them. We’ve mapped out how carbon prices are incentivising or disincentivising progress and innovation towards Net Zero across all major sectors of the UK economy. In this blog, we’ll explore how the average carbon price for aviation is currently subsidising emissions – instead of driving reductions – and what could be done about it.

Aviation emissions set to soar

By 2040, aviation will be the UK’s highest emitting sector, according to the Climate Change Committee. To reach Net Zero, the sector requires a dual approach: innovation in low carbon solutions, and carbon offsetting through robust greenhouse gas removals (GGRs). Currently, the sector is not getting the carbon price signals it needs to incentivise either of these.

The effective carbon price for aviation rewards emissions

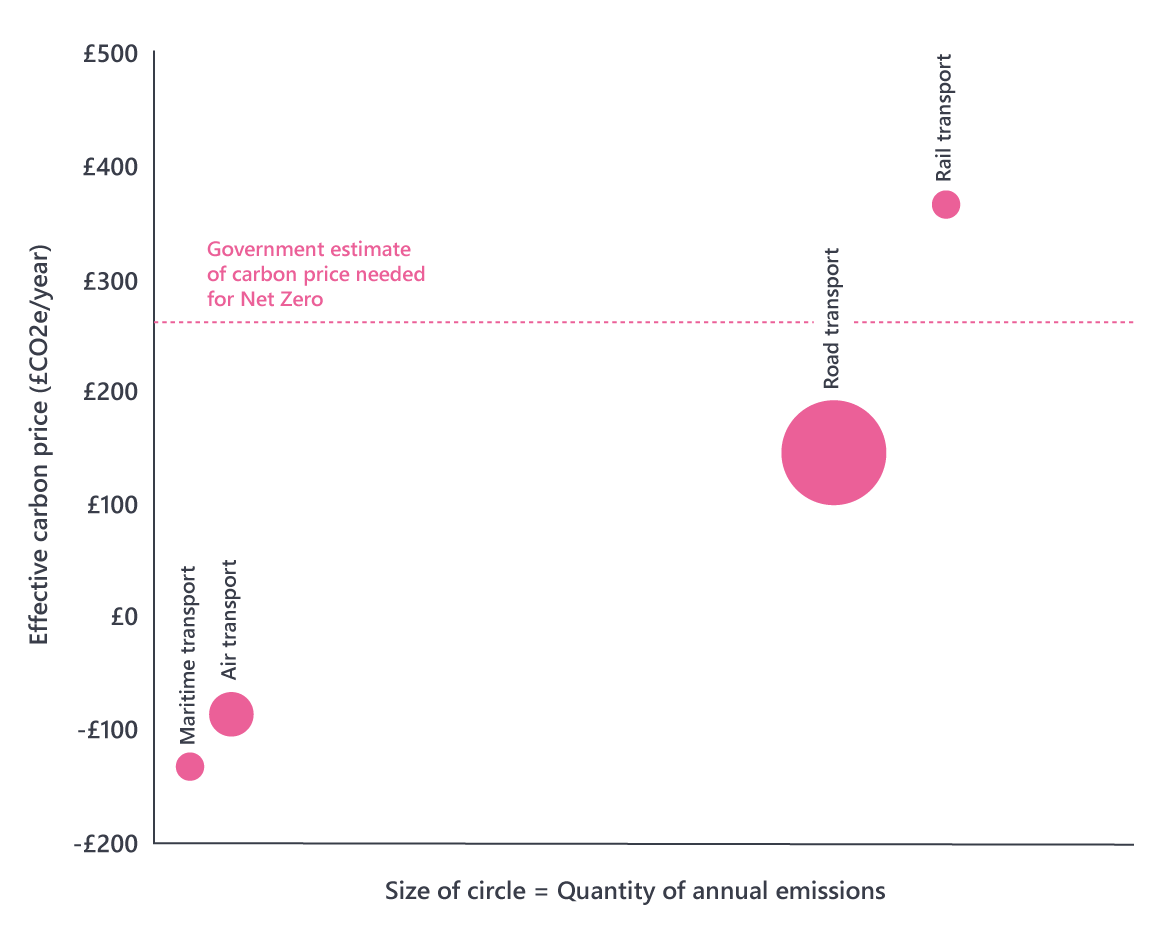

To calculate an effective carbon price, we add up the costs of both direct and indirect measures to find how much is paid for each tonne of greenhouse gas produced. For aviation, this is -£85/tCO2e. In this context, a negative carbon price means that airline operators are essentially being subsidised or rewarded for their emissions – whereas a carbon price above zero would represent a cost for their emissions.

The government has estimated that a carbon price of £261/tCO2e is needed to achieve Net Zero. Aviation’s effective carbon price is £346 lower than this – in other words, it is significantly underpriced. It is also significantly lower than the carbon prices for road and rail transport, as shown in Figure 1. Across all major sectors of the economy, the only sector with a lower carbon price than aviation is maritime transport (which will see its carbon price increase once its integrated into the UK Emissions Trading Scheme (ETS) in 2026).

So, what makes up aviation’s carbon price, and crucially, how could it be shifted to incentivise emissions reductions?

Figure 1. Effective carbon prices of different modes of transport.

What makes up the effective carbon price for aviation?

For aviation operators in the UK, there are several taxes, subsidies and schemes at play which factor into the effective carbon price.

Subsidies that reduce the effective carbon price:

Zero-rated VAT on fuel for planes. The UK is not alone in exempting jet fuel from VAT, with other countries doing the same under international agreements, but this is classed as an implicit subsidy by bodies such as the International Monetary Fund.

Zero-rated VAT on tickets. This subsidy makes up the biggest proportion of the ‘discount’ that aviation receives on its emissions.

Taxes and schemes which increase the effective carbon price:

Air Passenger Duty (APD). Charged on most passengers flying from UK airports, APD is calculated according to how far away the destination is, as well as the class of travel. To help bring aviation’s effective carbon price more in line with road or rail transport, APD could be increased (as was announced in the Autumn Budget 2024), or other passenger levies imposed such as a frequent flyer levy.

The UK Emissions Trading Scheme (ETS). Flights within the UK and Europe are subject to the UK ETS, which means that operators must pay for and surrender enough ETS allowances to cover their annual emissions. Currently, airlines receive a portion of their allowances for free, although this is set to end next year, which we expect will increase the overall effective carbon price.

The Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). CORSIA is a market-based carbon offset scheme run by the UN’s International Civil Aviation Organization (ICAO). Airline operators offset any emissions above a baseline, which is set at 85% of their 2019 emissions, by purchasing credits from carbon offsetting projects approved by the ICAO. This is currently voluntary but set to become mandatory from 2027 for airlines in the 193 member countries that are eligible based on economic development and amount of aviation activity.

Now we know which policies make up the effective carbon price for aviation in the UK, let’s look at how carbon pricing could incentivise the sector to begin its descent into Net Zero.

Low carbon technologies need to scale rapidly

Traditional jet fuel – kerosene – is very energy-dense, which makes it relatively difficult to replace in a sector where weight is king. Low-carbon options include:

Sustainable aviation fuel (SAF) made from synthetic fuels, biomass, or waste oil.

Liquid hydrogen.

Electric propulsion.

SAF, as the most mature of these technologies, is already blended into conventional fuel at low levels. The UK has an ambition for a network of SAF blending hubs with the first site expected to be operational by 2026. The Department for Transport has introduced the SAF Mandate, which stipulates that an increasing amount of SAF must be incorporated into jet fuel, beginning at 2% in 2025 and rising to 22% by 2040. The EU has a far more stringent target of 70% by 2040.

Currently, SAF costs between two and eight times more than kerosene – making it an unlikely choice for airlines in the absence of tougher mandates or higher carbon prices. Furthermore, SAF is predicted to face significant supply constraints, with global production not even meeting half of forecasted demand by 2035. Without rapid diversification and scale up of production methods, the SAF market will face considerable bottlenecks.

Encouraging greenhouse gas removals

With supplies likely to constrain SAF adoption, GGRs will be required to abate aviation emissions. The UK’s recent independent review of GGRs concluded that the sector “should be required to pay for the GGRs it needs to reach Net Zero…rather than spreading the costs across all taxpayers”.

It recommended changing the existing SAF Mandate to a ‘Net Zero Aviation Mandate’ to set a course for all out-bound flights to be climate-neutral by 2045. This would involve a combination of permanent GGRs and low or zero carbon fuels. Such a move, if it were implemented, could increase the effective carbon price for aviation.

Shifting passenger demand through frequent flyer levies

Consumer behaviour will also play a role in the sector’s progress towards Net Zero. 1% of the world’s population is responsible for 50% of the carbon emissions from commercial aviation. Levies could be applied to these frequent flyers, which would increase the average effective carbon price across the sector. France and Spain have joined a global coalition which proposes applying extra charges to business and first-class travel, as well as private jets. Consumers could also be incentivised through subsidies and discounts to use alternative modes of transport including trains.

A lack of international cooperation will hamper progress

Carbon pricing for aviation works best when it is joined up across borders. Global cooperation has been hampered by the stance of the current administration in the US, and some of the most polluting routes in the world – such as London to New York – are not covered by either the UK or the EU ETS. Whilst ICAO aims to cover global emissions, it does not have its own enforcement powers and is reliant on member states implementing obligations into their domestic legislation. There are also question marks over the willingness and ability of the US, Russia and China to compel their airlines to comply with CORSIA from 2027.

Furthermore, credits available under CORSIA are in short supply. To date, only one auction has been held, with credits available from a single scheme – a forestation project in Guyana. 11 airlines purchased credits. Estimates suggest that international demand for credits will reach between 100-182 million for CORSIA’s first phase up to the end of 2026, before surging to 0.5-1.6 billion during its second phase to 2035. Without a significant uptick in the number of credits available and a concerted effort from member states to implement obligations, CORSIA risks falling short of its ambition to place a global carbon price on flying.

Carbon pricing limited to fuel-use emissions

Currently, only emissions from the sector’s fuel use are covered by carbon pricing; yet it’s not the only source. For example, there are ‘contrails’, or ice clouds that form behind planes at high altitude as a result of water vapour accumulating around soot particles formed by burning jet fuel. Contrails have a significant warming effect, which is still being evaluated – and it has been suggested that minor changes to flight paths could reduce how many of them are produced. Pricing in other emissions sources would help increase the effective carbon price for operators.

An effective carbon price which is flying too low

The effective carbon price for aviation is currently flying too low to meaningfully incentivise emissions reductions. As we’ve discussed, several options exist for bringing it more in line with the carbon prices of other transport options, and other emissions-producing activities across the economy.

Without such measures, there’s a real concern that aviation will fail to reach its Net Zero destination.

Net Zero Carbon Policy

An Energy Systems Catapult thought leadership project, focusing on how the UK can develop an innovation-friendly, economy-wide framework for Net Zero.