Mixed signals for innovators: buffeted by war and a pandemic, the UK's effective carbon prices need rebalancing

Comment by Dr Danial Sturge, Carbon Policy Practice Manager at Energy Systems Catapult, and Leila Roberts, Economic Consultant at Stonehaven.

The UK has ambitious plans for decarbonisation: by 2030 all new cars should be electric or hybrid, and 600,000 heat pumps should be installed annually by 2028.

Yet our latest analysis shows that policies continue to send confusing signals to the market, ones that could deter clean energy innovators from launching products that help spark economic growth. The good news is that the tool and models we have developed can help inform more cohesive policymaking.

A fresh take on carbon pricing

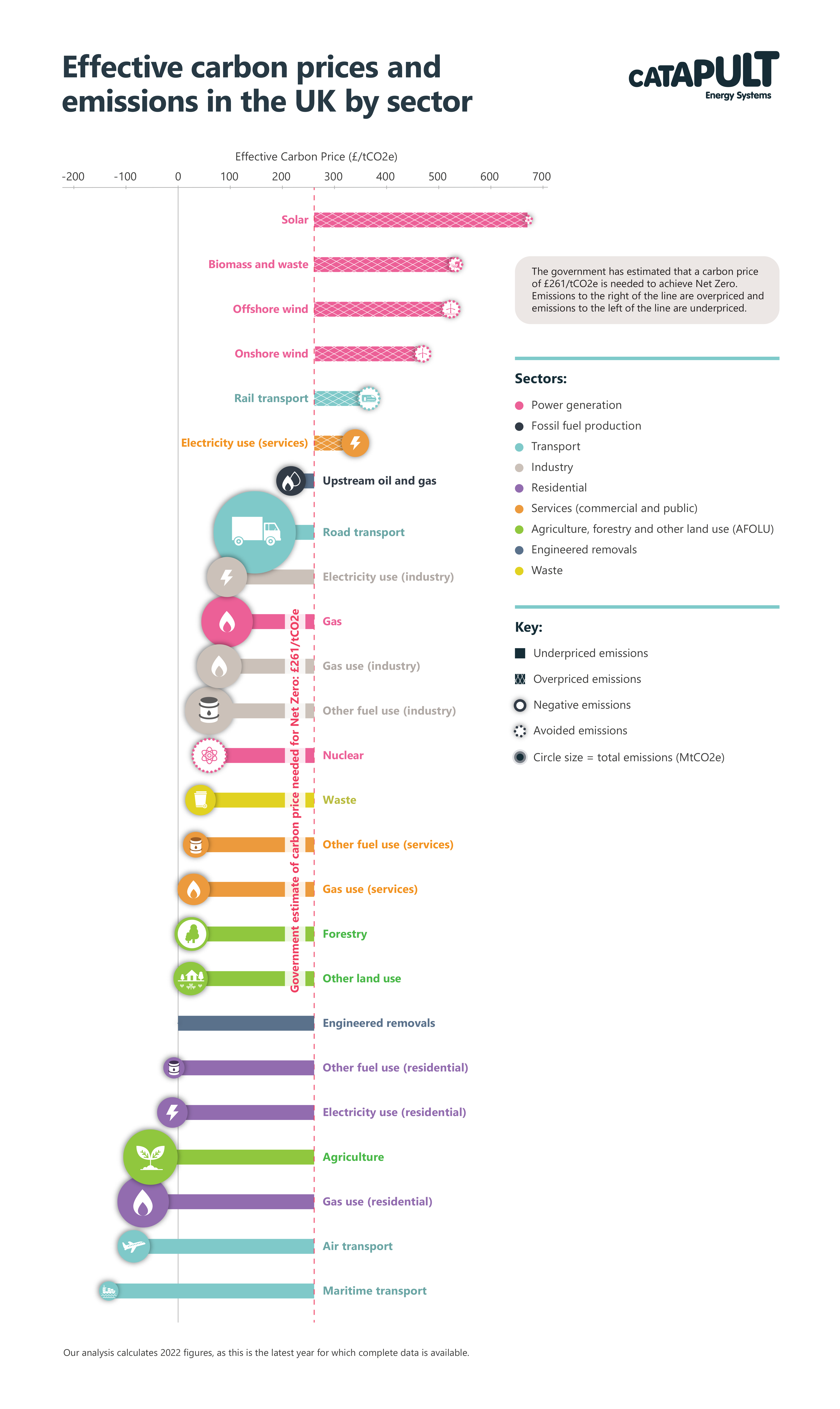

In 2018, Energy Systems Catapult published a snapshot of how the UK incentivises emissions reduction across the whole economy. We did this by calculating the ‘effective carbon price’ that emitting activities see:

The ‘effective carbon price’ is the incentive or reward for a business or individual to reduce emissions (in £/tCO2e) for a given activity (for example fuel consumption), resulting from the sum of carbon policies that are direct (for example explicit carbon pricing instruments, and energy and fuel taxation) and indirect (for example reduced VAT rate, and subsidies for low- and zero-carbon options).

Our analysis showed that, for the most part, we were significantly under-pricing emissions to drive the change and innovation needed to meet the UK’s Carbon Budgets.

While we updated the model in 2019, it has been left dormant since. But we now have a fresh, more detailed model, recently delivered by the team over at Stonehaven. We’ll discuss the insights from this update of our ‘economy-wide effective carbon prices dataset’ in more detail later, but first some important scene setting.

What has changed since our previous update?

In 2019, the UK led the way by legislating for Net Zero. Building on a previous target of reducing emissions by 80%, the UK legally committed that by 2050 any emissions are balanced by removals. Almost immediately this resulted in a shift in policy rhetoric, validated by the Johnson government’s manifesto that put Net Zero at its heart.

But the world quickly moved on:

2020 saw the Covid-19 global pandemic shift economic priorities.

Then in 2022, as the world had just begun recovering from economic lockdown, Russia invaded Ukraine which, among other things, sent gas prices soaring.

We continue to experience broader geopolitical tensions today, and all of this has influenced the extent to which policies encourage decarbonisation.

Our updated analysis provides a wealth of data, showing what makes up the total effective carbon price and the impact that individual policies have.

We intend to make the data and model publicly available, but for the purposes of this blog post, we have updated our simpler chart, which illustrates the weighted average of our various assumptions:

From this snapshot, we can see that most emissions are left of the line – they are underpriced. Indeed, all activities above the target price, except for electricity use in the service sector, are those that avoid emissions from fossil-fuelled alternatives such as renewable generation and rail transport. It appears to have been easier to reward abatement through subsidies than penalise emissions through tax.

This reflects how we’ve relied heavily on using mechanisms that support investment in the development and deployment of specific technologies for decarbonising the power sector.

At a macro level, this highlights how we have highly valued the emissions-reductions potential of renewables, while under-valuing emissions reductions in other parts of the economy.

This is broadly consistent with early Carbon Budgets, which focused on decarbonising the electricity system. But as we move into Carbon Budgets Six and Seven (covering the years 2033-2042) there’s a greater emphasis on decarbonising transport, buildings and industry, for which we need policies that more accurately value carbon in those underpriced sectors.

Furthermore, the chart shows that some emitting activities are significantly subsidised from an emissions perspective – they are priced below £0/tCO2e. Most notably gas use, but also the aviation, maritime and agriculture sectors.

Across the board, we can see that fossil fuel use remains undertaxed relative to electricity use.

Let’s dive a little deeper and look at the policy measures that have led to such a spread in effective carbon prices.

A cleaner grid and higher energy prices

As mentioned, electricity generation has been the focus of most government intervention to date. Here we see an interesting effect on our formulation of effective carbon prices: as we succeed in reducing the emissions intensity of the grid, each unit of subsidy for low carbon generation is divided by an ever-smaller emissions factor. The total amount of subsidies paid by consumers towards renewable generation in 2022 were broadly similar to 2018, but the carbon intensity of the grid fell by 40% during that time. This gives the impression that the effective carbon prices for those technologies are increasing. This also affects the end-users of electricity (residential, service and industry).

High energy prices have also fed through to the analysis. For residential gas customers, the effective subsidy has increased as higher prices have resulted in an increase in foregone VAT. Overall, both residential electricity and gas are now more underpriced compared to our previous analysis, largely because of an increase in foregone VAT from inflationary, real term increases in energy prices, and the absence of an explicit carbon price on gas.

More spending on low carbon activities

In rail, government subsidies have tripled since 2018/19, meaning rail has remained overpriced.

The land use sector has seen the creation of a new voluntary carbon market that rewards credits for restoring peatlands.

In forestry, while the level of sequestered emissions has remained largely the same, subsidies have increased over time, reducing the overall effective carbon price.

ETS, fossil fuels and farming

Direct carbon prices from emissions trading schemes (ETS) – first the EU Emissions Trading Scheme (EU ETS) and now the UK Emissions Trading Scheme (UK ETS) – are higher than before. UK ETS and Carbon Price Support (CPS) are estimated to have increased electricity prices from around 0.8p/kWh in 2016 (under the EU ETS) to 2.3p/kWh in 2022.

For industry, higher UK ETS prices feed through to an increase in the effective carbon price for both electricity and gas. Free allocation of UK ETS allowances limits the impact, however, for eligible sectors by reducing the overall effective carbon price seen by eligible industries.

In the case of fossil fuel production, rising oil prices have increased profits for producers and tax revenue for the government. This in turn has led to the introduction of the Energy Profits Levy, resulting in an effective carbon price aligned with the central estimate.

Since the Net Zero target was legislated, the understood importance of engineered removals has increased over time. While a new business model is under development, and proposals made for its future inclusion in the UK ETS, engineered removals do not currently have an effective carbon price.

For agriculture, the UK’s withdrawal from the EU and its Common Agricultural Policy, has led to the introduction of environmental-linked payments – not all of these are targeted at emissions reduction. The inclusion of red diesel in our analysis means the agricultural sector is now more underpriced, though this has been countered by the introduction of an environment-linked farming payment.

Transport going nowhere

In road, taxes – notably Fuel Duty – have remained frozen or even been cut (albeit temporarily). Methodological updates have also halved the estimated cost of congestion, meaning our calculations deem government policy to be more targeted at emissions. A combination of these factors means that despite relatively heavy taxation, road transport is underpriced from a carbon perspective.

In aviation, we see the aftermath of Covid-19 in the fall in the lower price estimate: while aviation emissions fell by 25%, air fares were around 25% higher in 2022 than their pre-pandemic average. This is likely due to pent up demand. An increase in the higher fares means higher foregone VAT, which in turn implies that carbon emissions in aviation are underpriced even more than in our 2019 analysis.

In waste, while annual emissions from landfill have remained steady in the interim years, landfill tax revenue has fallen, leading to a lower effective carbon price.

In summary

Sending price signals reflective of the UK’s Carbon Budgets and Net Zero target is essential for enabling innovation. If the UK continues to incentivise polluting technologies or services over the low carbon equivalent, then innovators across the economy will be unable to bring their products to market.

Low carbon products and services not only reduce emissions, but improve upon the status quo for consumers. Levelling the playing field by rebalancing effective carbon prices is an important part of the tool kit for providing businesses the opportunity to thrive in an ever-changing, competitive landscape.

In this blog we have looked across the economy at a high level, but there is still plenty to glean from looking at sectors in greater detail, which we will begin to do in our upcoming blogs on residential heating and industry.

Looking ahead, we purposely designed our model so that it can be updated over time – whether it be with the latest published data or inclusion of completely new policies. This will reveal how policy design impacts the strengths of carbon price signals considering external factors (such as international gas prices and global demand for air travel). Ultimately, this stresses the need for new tools to inform cohesive policymaking.

Net Zero Carbon Policy

An Energy Systems Catapult thought leadership project, focusing on how the UK can develop an innovation-friendly, economy-wide framework for Net Zero.