Mixed signals: UK industry needs a clearer path towards decarbonisation

Comment by Emily Ford, Senior Energy Policy Advisor – Carbon Policy

Carbon pricing helps businesses understand the cost of their emissions and make commercially informed choices about reducing them. To drive meaningful action, these price signals must create incentives for low carbon options. Doing so also removes the barrier to entry for innovators of low carbon products.

Yet, current carbon price signals for UK industry are mixed. We’ll look at:

how current carbon prices discourage industry from switching from gas to electricity;

what impact the UK Emissions Trading Scheme (UK ETS) has on carbon prices for industry;

why some industrial sub-sectors are rewarded more highly than others for reducing their emissions.

Calculating an effective carbon price

Energy Systems Catapult first set out to explore how carbon prices measure up across the economy in 2018/19, and now, with Stonehaven, has delivered a major update to its dataset and is publishing this new analysis to help understand the signals that carbon policies are sending to different sectors.

To calculate an effective carbon price, we add the costs of direct measures (like carbon taxes or fuel duties) with indirect ones (like reduced VAT or subsidies for low carbon options), to find how much an emitter pays for each tonne of greenhouse gas they produce. For UK industry, these prices vary widely between sub-sectors depending on emission sources and available exemptions.

Overall, industrial emissions remain significantly underpriced compared with the £261/tCO2e that the government estimated in 2022 was needed to achieve our Net Zero obligations.

Energy emissions: comparing electricity to gas

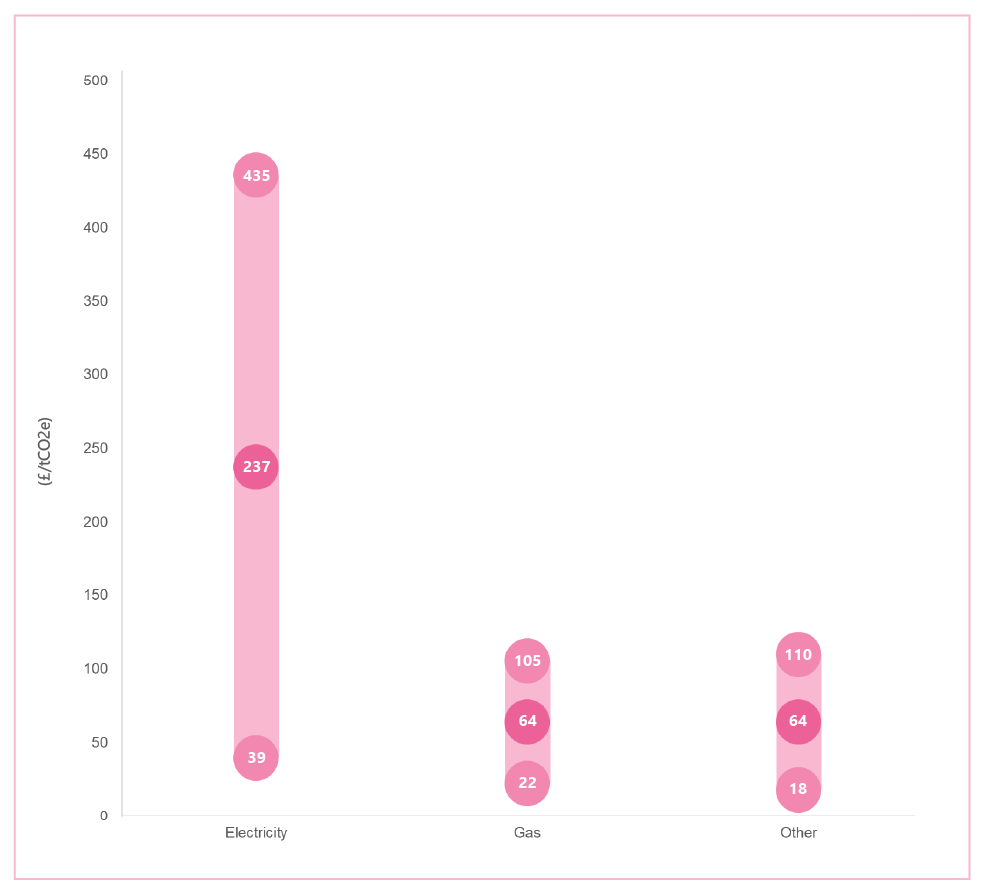

If industry is to reduce its emissions from using energy, it needs to move away from unabated fossil fuels to lower carbon options, such as electricity. Currently, the incentive to do so is hampered by the ‘spark gap’, which is the high cost of consuming electricity relative to gas. This is compounded by electricity also having a significantly higher effective carbon price than gas – which serves as another disincentive for industry to make the switch. The effective carbon price of electricity for industrial users is 3.7 times greater than the effective carbon price of gas, at £237/tCO2e compared to £64/tCO2e (see the mid-point values in Figure 1).

Figure 1. Effective carbon prices of different industrial energy sources in 2022: High-point, mid-point and low-point (£/tCO2e)

Compensation schemes are a decisive factor in electricity’s effective carbon price

The ‘spark gap’ is partly due to support mechanisms for low carbon electricity generation, which are funded through additional costs on consumers’ bills. Industry has access to several exemptions and compensations for these costs:

Energy Intensive Industries (EII) schemes, which compensate industry for certain indirect costs by passing them onto other consumers.

Climate Change Agreement (CCA) discounts available on the Climate Change Levy (CCL);

Network Charging Compensation (NCC) scheme.

Such schemes not only bring down industry’s electricity bills – but also have an impact on the effective carbon price paid for in their electricity use. Without including any exemption or compensation schemes, the effective carbon price for electricity rises to £435/tCO2e (the high-point value in Figure 1). Conversely, including all subsidies to the maximum possible coverage brings the effective carbon price down to £39/tCO2e (the low-point value in Figure 1). Different industrial sub-sectors may or may not be eligible for these compensations, which contributes to different carbon prices between them. We’ll discuss this in more detail later.

More electricity subsidies coming

In its Industrial Strategy, the government announced a British Industrial Competitiveness Scheme, due to be launched in 2027. It aims to reduce the cost of electricity by £30-40/MWh for eligible businesses, exempting them from paying policy costs including the Renewables Obligation (RO), Feed-In Tariff (FIT) and Capacity Market costs. The Industrial Strategy also included an uplift in the NCC scheme from 60% to 90% compensation from 2026.

These announcements have been widely welcomed by industry, but subsidies in the form of compensation and exemptions will not be sustainable forever. Other policy levers are needed to reduce system costs and make widespread electrification more economically viable. In the aftermath of the decision against zonal pricing under the Review of Electricity Market Arrangements (REMA), the question remains as to how government will reduce electricity costs for industrial (and other) consumers in the long-term.

Moving policy costs from electricity to gas

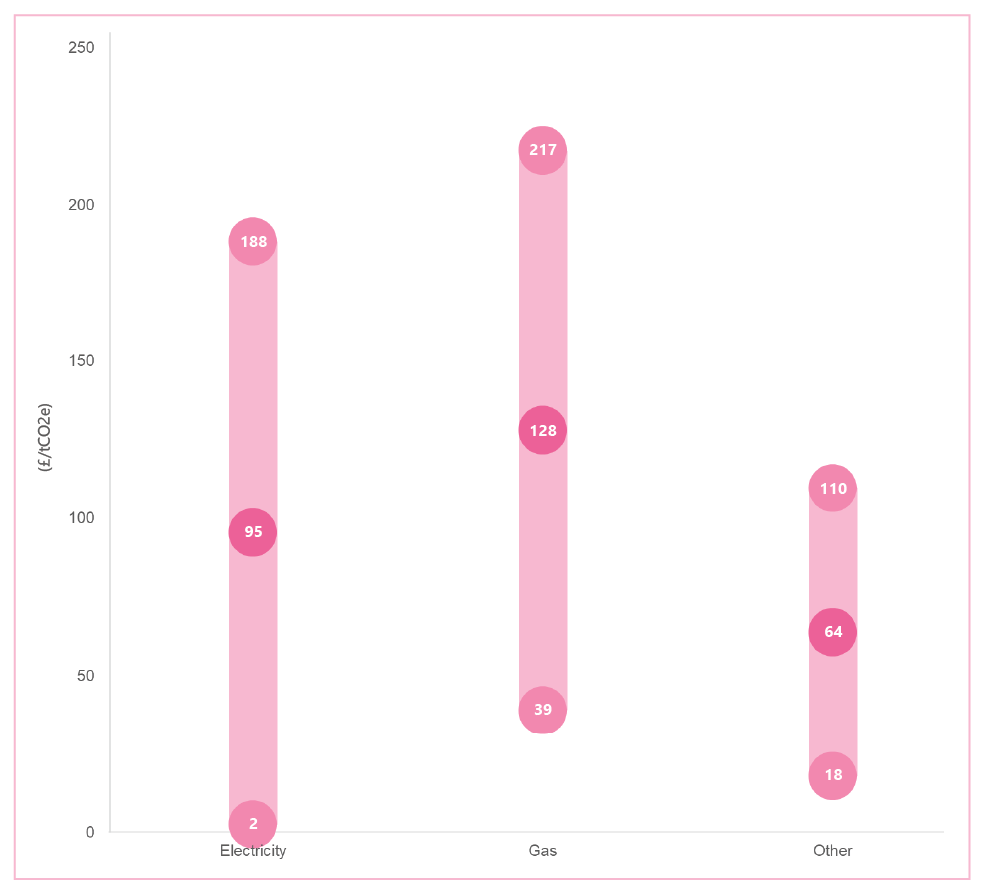

Given the government’s current focus on reducing policy costs for industrial electricity use, we wanted to model the impact of this on the effective carbon price. As Figure 2 shows, removing historic policy costs (specifically the RO and FIT) from industrial electricity bills would bring down electricity’s effective carbon price from £237/tCO2e to £95/tCO2e. Removing these costs from industry’s electricity bills means, of course, that they must be borne elsewhere. This could be through general taxation – or by moving them onto gas bills. The latter would result in gas’ effective carbon price doubling from £64/tCO2e to £128/tCO2e.

To truly incentivise a shift away from fossil fuel energy, policy changes will be needed to bring the effective carbon prices of gas and electricity into balance.

Figure 2. Effective carbon prices for industrial energy if FIT and RO costs were moved from electricity to gas (£/tCO2e)

Pricing process emissions in the UK ETS

The UK ETS applies a direct carbon price to industrial process (Scope 1) emissions, by requiring in-scope industrial operators to surrender allowances equivalent to their annual emissions. Allowances can be purchased, but are also given for free to sectors which are judged to be at risk of carbon leakage.

Our analysis estimates that industrial activity covered by the UK ETS produced 43 million tCO2e of emissions in 2022. The same year, industry was granted free allowances covering 32 million tCO2e, providing a significant discount of 76% on the effective UK ETS price.

Free allowances act as a brake on emissions reductions

Free allowances can be traded so participants are incentivised to decarbonise their processes if the value of free allowances is higher than the cost of reducing emissions. In reality however, it may be less of a priority for businesses to decarbonise if their free allowances cover a significant proportion of their total emissions.

Once the UK’s Carbon Border Adjustment Mechanism (CBAM) is introduced in 2027 to mitigate the risk of carbon leakage, we hope to see fewer free allowances being granted. This would strengthen the incentive to decarbonise. The effective carbon price for the chemicals sub-sector, for example, would move from £29/tCO2e to £67/tCO2e if free allowances were removed.

Accurate emissions reporting is a must

For the CBAM and other carbon policies to be effective, industry and government need access to accurate and robust emissions data. The current regulatory landscape for emissions reporting is fragmented and complex, and more standardisation is needed within carbon accounting methodologies.

Our proposal for an economy-wide Carbon Regulator seeks to address these challenges and to ensure that industry and government have the data they need to make the right decisions about decarbonisation pathways and low-carbon products and processes.

Effective carbon prices across industrial sub-sectors

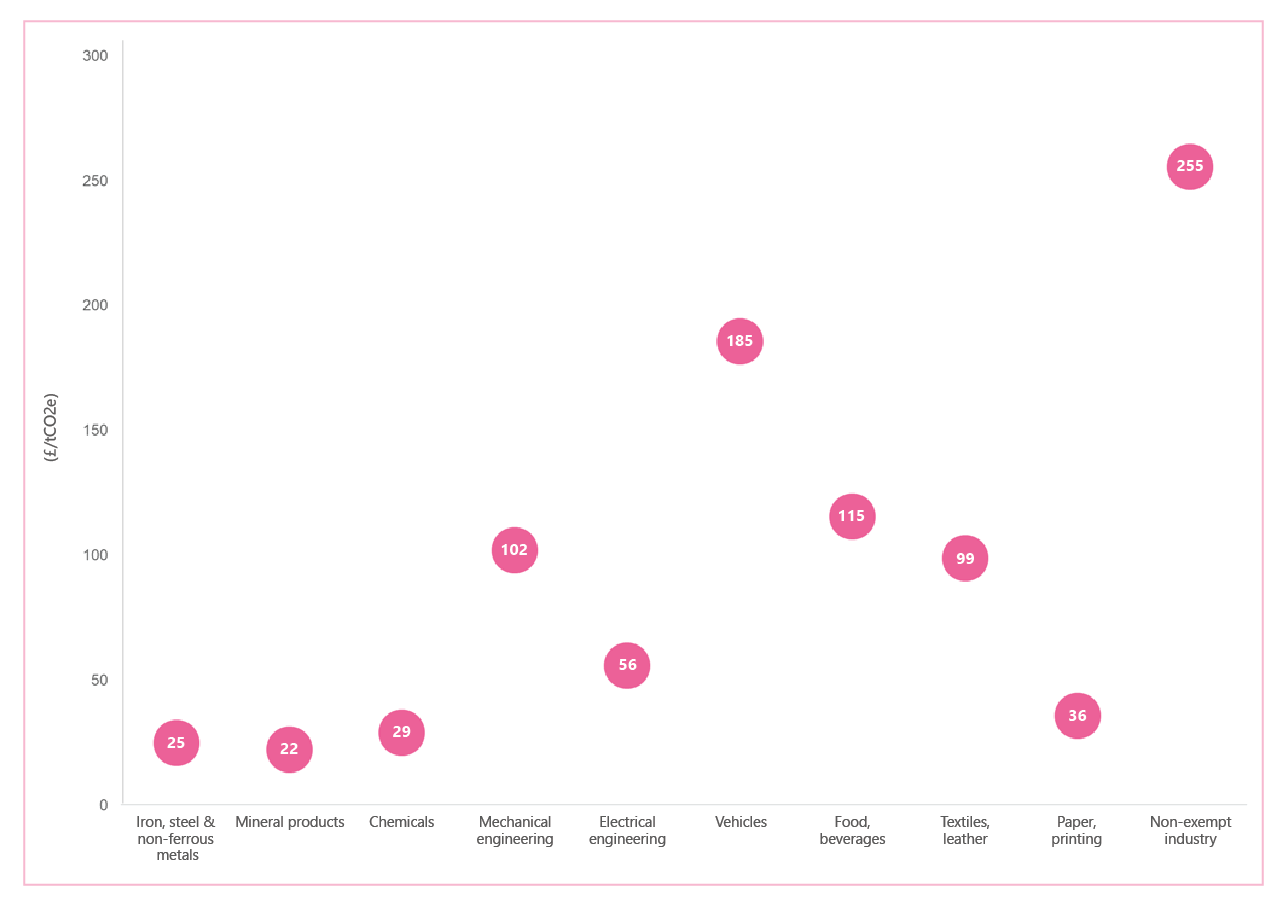

Effective carbon prices vary significantly between different industrial sub-sectors, as shown in Figure 3. This is due to a complex landscape of subsidies and exemptions. These sub-sectors also differ regarding the extent of trade exposure, the decarbonisation options available to them and whether emissions are mostly produced from fuel use or directly from industrial processes.

Figure 3. Average effective carbon prices by industrial sub-sector (£/tCO2e)

Foundational industries lack strong signals

The sub-sectors in which carbon is most undervalued are:

Mineral products

Iron, steel and non-ferrous metals

Chemicals

Paper and printing

These are some of the UK’s foundational industries, which, together with the glass and ceramics subsectors, produce 28 million tonnes of material each year and are worth £52 billion to the economy. Comparatively low effective carbon prices mean that these sub-sectors are not being rewarded as much as other sectors of the economy for their emissions reductions.

Notably, most emissions from mineral products (including cement) are process emissions, which have fewer decarbonisation options. Such installations are likely to rely more heavily on carbon capture and storage (CCS), which faces technological, market-based and infrastructural hurdles.

Other subsectors are rewarded for emissions reductions

At the other end of the spectrum, the manufacture of vehicles is subject to a far higher average carbon price, as are food and beverages; mechanical engineering; and textiles and leather.

The food and beverages, and mechanical engineering sub-sectors stand out as being more reliant on gas, whereas vehicle manufacture and textiles both have a more even split between gas and electricity use. Low-temperature processes within these subsectors could make them good candidates for moving away from gas to electrification.

Finally, in Figure 3 we have non-exempt industry representing installations that are not eligible for support under the CCA, EII or NCC schemes, and are therefore subject to a significantly higher effective carbon price. Across all other subsectors with their varying exemptions, the mean effective carbon price in 2022 was £74/tCO2e, compared to £255/tCO2e for non-exempt operations.

Effective carbon prices signpost the route to Net Zero

This decade and the next, the UK will have to make substantial progress in decarbonising industry. This comes with several challenges, including:

tackling carbon leakage;

understanding the different pathways for industrial clusters and dispersed sites;

developing hydrogen and CCS networks.

Meaningful carbon price signals have a crucial role to play in incentivising progress, including innovation. The current patchwork of subsidies and exemptions means that these signals are not always working in favour of decarbonisation, particularly when it comes to the ‘spark gap’.

Policy must address the relative carbon price of electricity versus gas use and ensure clearer price signals across sub-sectors to accelerate industry’s journey to Net Zero.

In the final blog of this series, we’ll look at the signals that effective carbon prices are sending for residential heating.

Net Zero Carbon Policy

An Energy Systems Catapult thought leadership project, focusing on how the UK can develop an innovation-friendly, economy-wide framework for Net Zero.