Watts the story? (October 2025) – Ben Shafran

If you’re developing a consumer-facing energy proposition, have a technology that can provide flexibility to the system, or support electricity networks with their investments and grid operations, my summary below of three recent announcements from the energy regulator Ofgem will help you keep up to speed with important changes.

High energy costs continue to be near the top of the political agenda. The latest data from the Department for Energy Security and Net Zero shows that, among rich countries, the UK continues to have the highest electricity prices for industry and the second highest prices for households (after Germany). So, you can understand the urgency that Ofgem, whose primary duty is to protect consumers’ interests, must feel to act.

What approach did Ofgem take? It announced that retailers will be required to offer consumers a low (or zero) standing charge. Ofgem’s press release presents this as a done deal but it is, in fact, subject to public consultation and stakeholders have until 22 October to respond.

The move has been widely criticised by the energy sector (see, for example, Energy UK’s response). The timing is particularly baffling as it came on the day Ofgem closed a broader consultation on how retail electricity tariffs should be structured. Putting myself in the shoes of clean energy innovators, I’d have two concerns:

Our response to Ofgem’s consultation on allocating electricity system costs makes the case for an entirely different approach, one that is anchored in what we call ‘regulatory diversity’ – where the regulatory burden is proportionate to the different level of risk that different consumer propositions carry. Doing so will enable a highly competitive and innovative market for consumer propositions.

Our future clean power system will require storage technologies that boast different technical characteristics and durations of operation to effectively meet the gaps between when renewable generation is plentiful and when demand is high. Our Chief Technology Officer, Jon Saltmarsh, explains the different types of “peak gaps” in this blog.

The market for short-duration flexibility is quite well served by demand-response and batteries that respond to signals from local and national markets. But the government has identified the need for a dedicated support scheme to encourage investment in longer-duration storage. This has led to the creation of a ‘cap and floor’ scheme – modelled on the scheme that underwrites investment in interconnectors.

In the simplest terms, the scheme guarantees a minimum level of revenue for qualifying projects (the floor), with a quid pro quo that revenues above a certain level (the cap) are returned to consumers.

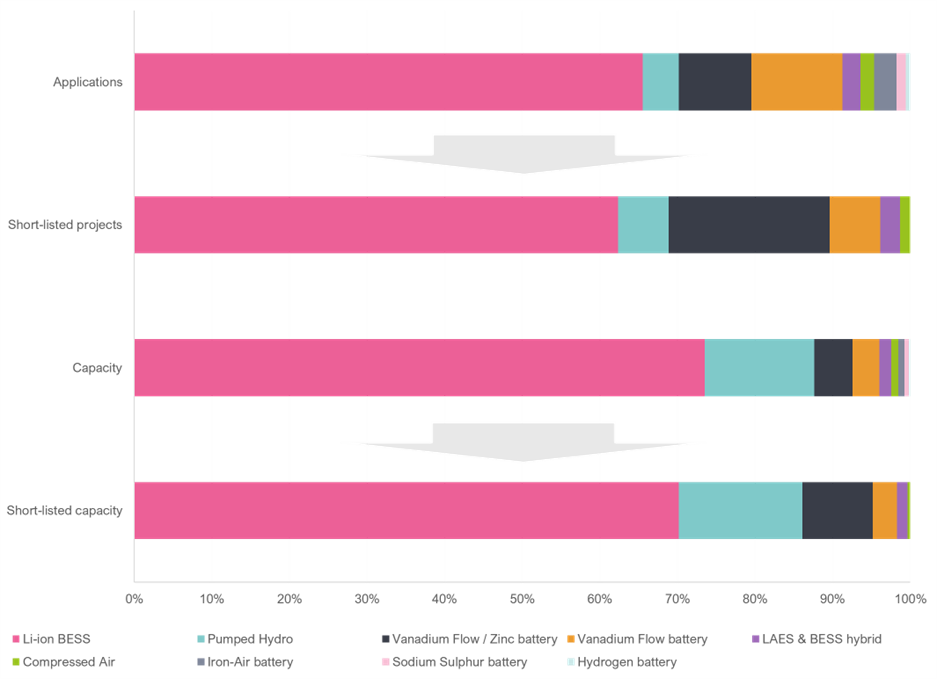

The first applications for projects seeking to participate in the scheme resulted in 171 applications. Ofgem has announced that 77 of these have passed the first qualification phase and will now be subject to a more detailed cost-benefit analysis informed by NESO modelling.

The data (see Figure 1) offers early insights into which technologies are likely to do best under the scheme’s current design, which requires a minimum operational capability of eight hours dispatch.

Applications and short-listed projects were dominated by lithium-ion batteries. They made up:

By storage capacity, they made up:

Meanwhile, pumped hydro storage had the largest capacity per individual project. The five out of eight pumped hydro storage applications shortlisted by Ofgem make up 16% of total short-listed capacity.

Figure 1: Energy Systems Catapult’s visualisation of figures presented in Ofgem’s LDES eligibility assessment

The cap and floor scheme is likely to direct the vast majority of investment in longer-duration storage, much as Contracts for Difference have done for renewable generation. As currently constructed, it may not secure enough capacity for what is called ‘very long duration storage’ which is needed to bridge the ‘peak durational gap’ that Jon Saltmarsh discussed here. We are working on these issues as part of our Innovating to Net Zero project and will share our insights in the coming months.

Ofgem has set out its detailed thinking on how it will approach the next regulatory period for electricity Distribution Network Operators (DNOs). Known as ‘ED3’, it will run from April 2028 to March 2033, coinciding with what is expected to be a significant uptick in investment in the local electricity grids.

Ofgem’s dominant theme for ED3 is planning. The DNOs will be tasked with producing ‘integrated network development plans’ to 2050 and base their investment plans for ED3 on that outlook. Those plans will use inputs on electricity demand and supply forecasts from NESO’s ‘transitional Regional Energy Strategic Plans’ (tRESPs). NESO recently shared its initial insights into tRESPs here.

The ED3 consultation, which runs until 3 December, reinforces Ofgem’s view that the priority in ED3 is to accelerate and scale up investment in the local grids. This represents a shift from its current approach, which Ofgem characterises as “flexibility first”. In previous submissions to Ofgem, we have argued that flexibility should continue to feature prominently in ED3 because it helps with prioritising grid reinforcement projects, supports system efficiency, and provides resilience against low-probability / high-impact events.

Ofgem has also confirmed that the innovation funding for ED3 will be made consistent with the approach for the other energy networks, whose next price control period runs from 2026 to 2031.

In particular, a newly launched Energy Networks Innovation Taskforce will set out long-term innovation challenges, and innovation projects would need to be aligned to these challenges to receive funding from Ofgem’s Strategic Innovation Fund. Energy Systems Catapult is pleased to be part of the Taskforce. We will be advocating the role that clean energy innovators can play in helping to resolve the emerging challenges facing the sector.

Independent and technology-agnostic markets, policy & regulatory thought leadership tackling the hardest challenges on the way to Net Zero

Find out moreFind out more about how Energy Systems Catapult can help you and your teams

Find out more about how Energy Systems Catapult can help you and your teams