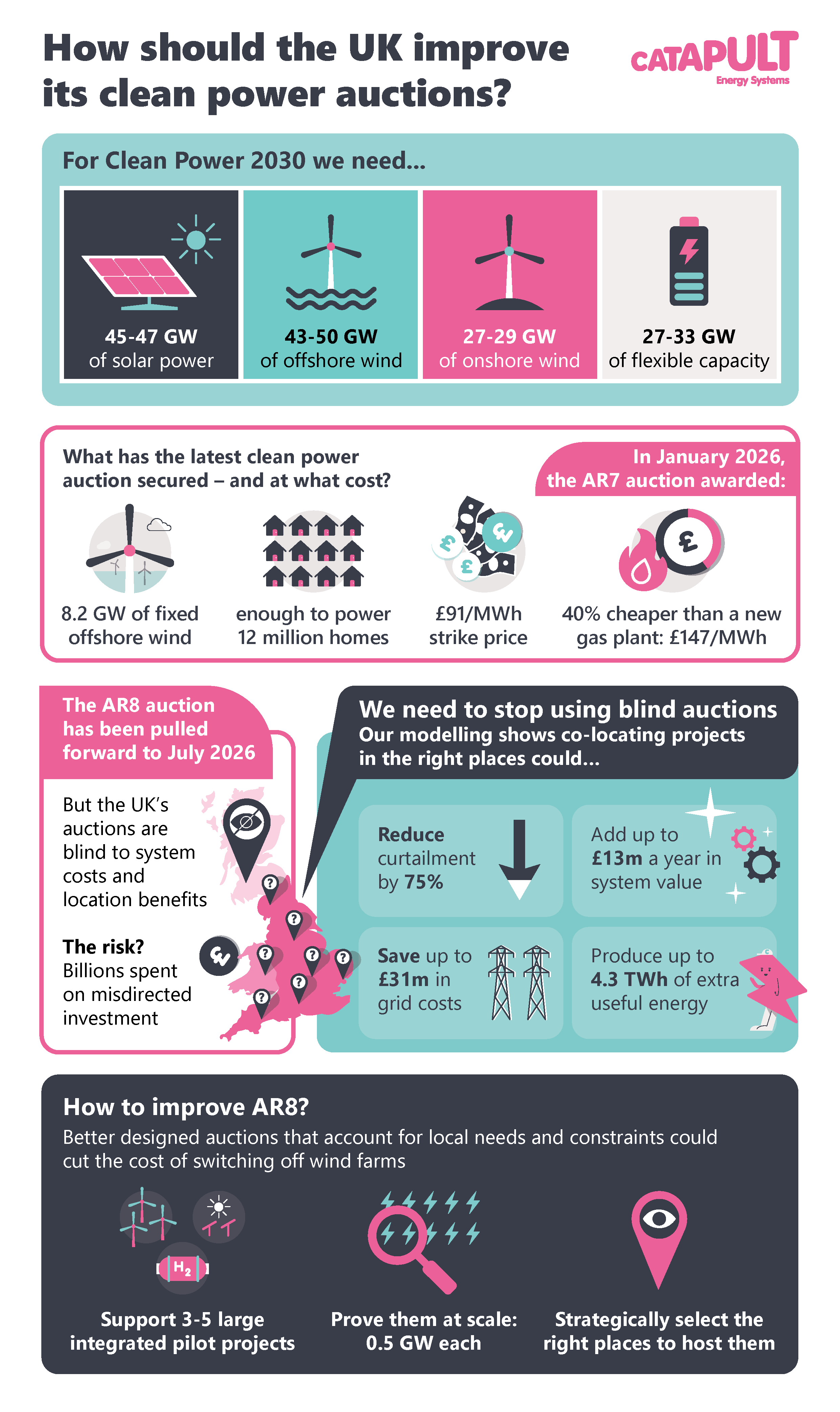

Renewable energy is being added to the grid without fully considering how it affects the wider energy system, or what the trade-offs might be. The allocation round 7 (AR7) auction for future offshore wind gave the UK momentum, speeding us towards a cleaner energy system by 2030. But without a sharper focus on integrating and co-locating innovative technologies, grid constraints will slow electrification to a crawl, adding billions in energy system costs.

With the UK government announcing that the next auction (AR8) has been brought forward to July to boost clean power deployment and strengthen our energy security, designing auctions that value co-location and energy system benefits has become even more urgent. Based on our latest modelling for the Hydrogen Innovation Initiative we are calling for immediate changes to AR8.

First, there’s a need to create strategic innovation zones, where technologies like wind, hydrogen generation and storage can be co-located to maximise energy output and drive down network costs.

Also, tweaking AR8’s Contracts for Difference (CfD) so that the scheme can reward projects built to benefit the whole system, not just for the capacity they’ll add.

AR7 – a momentum shift

Before exploring what’s needed for the next auction, let’s go through a quick recap on the previous one.

AR7 secured 8.4 GW of offshore wind at competitive prices, reaffirming that the CfD model can still deliver scale even after a turbulent AR5.

Fixed‑bottom offshore wind projects cleared around £90-91/MWh, significantly below the cost of new gas generation, and investor confidence recovered as the government introduced 20‑year contract terms that better reflect inflation and supply‑chain pressures.

This matters because the government’s Clean Power mission requires the system to meet 95% of annual demand with generation from low-carbon technologies by 2030. This means the UK needs to quadruple its operating or committed offshore wind capacity to 43-50 GW by the end of this decade.

AR7 puts us on that path, but it also exposes a structural gap. CfD remains location neutral, rewarding the lowest‑cost bids regardless of where projects land.

Without a coherent co‑location and system integration strategy, much of this new capacity risks getting stuck behind grid bottlenecks, leading to slower connections, rising system costs and higher rates of curtailment.

Industry has warned that unresolved grid constraints and an unfit for purpose transmission charging regime could restrict competition and system value in AR8, particularly in Scotland.

We can’t keep treating renewables, hydrogen, energy storage and offshore technologies as siloes. This is where co-location and integration stops being a nice to have and becomes an essential part of the operational model.

With AR8 now accelerated, developers face compressed timelines that risk reinforcing system-blind siting decisions unless integration and flexibility are explicitly rewarded in the next round.

What is co-location, and what are the modelled benefits?

Our latest Innovating to Net Zero analysis shows that, as things stand, the UK will not reach Net Zero in the most cost-effective way.

We will reach Net Zero affordably only when renewables are paired with flexibility, including storage, smart demand, hydrogen, hybrid offshore technologies and digital coordination – so the system can absorb variability and meet rising peaks in electricity demand.

To put this in context, the rapid growth of electric vehicles (EVs), heat pumps, data centres and industrial electrification could see electricity demand increase by as much as 80% by 2040.

Our modelling of the energy system shows that deployment of renewable capacity, enabled by low-carbon flexibility has the lowest system costs – with total savings of at least £70 billion by 2050. Strategically co-locating technologies could be one of the most powerful tools in our arsenal for achieving this.

Co-location in practice means placing complementary technologies side‑by‑side so they operate as a single, flexible energy system. An offshore wind farm might be paired with a floating solar array, wave or tidal devices that boost output and smooth variability.

An onshore wind site could host electrolysers, battery storage, industrial loads, or port operations that use power locally rather than pushing everything onto constrained transmission lines.

By clustering generation, storage, and demand in one place, co-located projects reduce curtailment, cut grid costs and improve the use of every megawatt produced.

Modelling finds big savings

The Catapult’s Co-Location Model (CLM) was developed to explore how flexible technologies interact within an integrated energy system.

Instead of optimising individual technologies in isolation, the model simulates how generation, storage, flexible demand and network limits interact over time.

This allows different combinations of infrastructure to be tested under realistic system conditions.

Our findings are clear: adding infrastructure in isolation often provides little additional value, while adding flexibility or coordination can transform system performance.

When projects make use of local demand or storage, the risk of delay, curtailment or negative pricing is materially lower. When they’re located in zones with grid headroom, the chances of timely grid connection are higher. When they incorporate hybrid offshore technologies, their output profile becomes smoother.

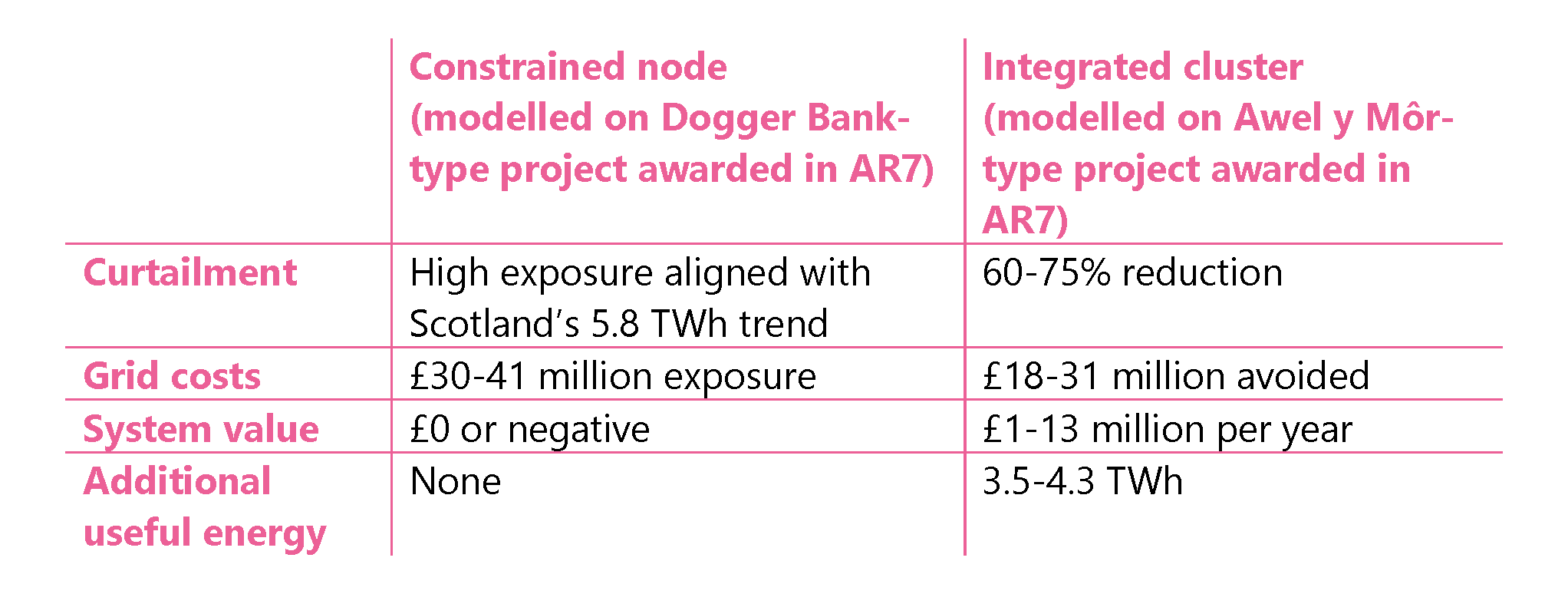

Based on modelled scenarios from Energy Systems Catapult’s CLM, co‑locating offshore wind with local flexible demand can reduce curtailment by 60-75%. Because this energy no longer needs to be constrained or redispatched, the system avoids an estimated £1-13 million in grid‑related costs per GW each year. The same modelling shows that several terawatt hours of additional energy become available for productive use compared with a standard export‑only offshore wind configuration.

The table below shows how two AR7-type offshore wind projects with identical £91/MWh strike prices can deliver very different system value depending on their location, grid constraints and the extent of integration.

Dogger Bank and Awel y Môr are used here as illustrative examples of offshore wind projects in constrained versus integration-ready locations. All figures represent modelled ranges based on system-level data, not project specific operational outcomes.

Figure 1: System impact of offshore wind projects depending on location and integration. (Grid cost values are indicative per‑GW ranges based on location, modelled for high‑constraint vs co-located low‑constraint scenarios using SSEN zones and DESNZ CfD methodology. All system‑value figures are derived from the CLM and associated Innovating to Net Zero modelling. Values represent modelled ranges, not project‑specific audited outcomes).

How do we unlock this value by tweaking AR8?

If you’re sitting in the Department for Energy Security and Net Zero (DESNZ), NESO, a devolved administration, a local authority or an industrial cluster team, you might be thinking: “Okay, I get the challenge. But what do we actually do next?”

This isn’t about ripping up the CfD rulebook or reinventing the planning process. It’s about a handful of smart, deliberate shifts – enough to fit within existing frameworks but powerful enough to steer 50 GW of offshore wind towards the places and configurations that deliver real system value.

Earmark some strategic integration zones

We need to clearly identify where integrated projects belong because offshore hubs (North Sea, Celtic Sea) and onshore industrial clusters (Humber, Teesside) are not equal in system terms.

Right now, every offshore project enters the allocation rounds on equal terms, regardless of whether it lands:

- in a heavily constrained onshore node;

- next to a port with industrial demand that needs flexible power;

- in a hybrid‑energy hotspot;

- in a region where curtailment already costs millions of pounds a day.

We know these places are not equal from a system perspective. The first pragmatic step we should take is designating five to seven ‘Strategic Energy Integration Zones’.

Not new structures, not a planning overhaul – just a clear, evidence-based signal that these are the places where integrated wind, storage, hybrid offshore technologies and local demand create the biggest system value from co-located and integrated offshore projects.

Our Wind electrolyser spatial work in collaboration with Ricardo, already shows where co‑location delivers the biggest wins.

In these Strategic Energy Integration Zones, we should fast-track nationally significant infrastructure projects (NSIPs), grid headroom and relevant consents. We should also align NESO’s network planning with devolved and local priorities so that developers, authorities and system planners are working from the same map.

De-risk demonstrations

Second, we need a UK-scale demonstration step that makes integration the norm rather than the exception – and gives investors the stability and replicability needed to back projects.

While the offshore industry is capital intensive and sensitive to risk, the innovation curve has moved. The technologies that make co-location possible are no longer theoretical – they’re bankable and scalable.

Existing projects in Europe prove these points:

- Hywind Tampen combines floating wind with offshore platform demand.

- Sinn Power integrates wave-solar hybrids.

- Minesto demonstrates tidal generation paired with microgrid flexibility.

AR7 moved in the right direction with 20-year CfD terms, strengthening bankability for projects that integrate additional technologies – but targeted support for UK scale-up remains the missing piece.

The Hydrogen Innovation Initiative addresses this directly, proposing a sandbox fund for AR7/AR8 integration that supports co-location with storage, port bunkering, industrial demand and multi-vector hybrids.

A targeted programme of first-of-a-kind co-location hubs, developed within designated Strategic Energy Integrated Zones, would turn existing proof-of-concepts into replicable domestic practice, de-risking AR8 and beyond.

The benefits here are significant. Our modelling shows that hybrid offshore platforms, integrated with floating solar arrays, tidal or wave technologies, can deliver a 60-75% capacity uplift.

This makes a compelling case for creating three to five large-scale integrated pilots, each around 500 MW, in the right locations.

If you’re shaping policy, this would be the difference between uncertainty and investment clarity.

If you’re a local authority or devolved administration, it gives you a playbook to anchor regional growth plans.

And if you’re in the industry, it provides the replicable design patterns needed to reduce risk, secure financing and accelerate deployment.

Evolve CfD to deliver more system value

At the moment, CfD does a brilliant job of securing the lowest cost generation, but it’s completely blind to system value.

With AR8 brought forward, developers have less time, there’s a higher risk they’ll bid to put projects in constrained regions, and greater probability of locking in curtailment and system costs for 20 years.

We know that curtailment is one of our most urgent risks in achieving Clean Power 2030. Large volumes of wind production, particularly in Scotland, are routinely curtailed due to grid constraints. Megawatts are being procured that the system already knows it may not be able to use effectively.

If we don’t integrate flexibility into AR8, we will pay the price twice: once to build the wind farm, and again to turn it off.

This is the system telling us that we cannot afford to keep adding generation into bottlenecks.

NESO’s connection queue reforms reinforce this: projects that relieve constraints will move faster, while projects that worsen constraints will slow down. And with AR8 now happening sooner, these queue reforms will shape which projects can realistically participate, favouring those that reduce constraints rather than worsen them.

Floating wind, which will dominate new capacity in the coming years, only intensifies the issue. Floating sites are often far from load, require port readiness, and come with complex consenting and geographic challenges. If they’re not integrated with flexibility, hybrid technologies or local demand, they risk becoming stranded generation.

Our MarineWind analysis on the viability of co-locating floating offshore wind with tidal, wave and hydrogen systems shows that in constrained regions like Orkney, tightening network constraints shift the optimal configuration away from maximising generation – towards combinations that enable local use, storage and reduced curtailment.

In short, co-located assets reduce system stress, improve asset utilisation and deliver more resilient investment outcomes. They shift the optimal mix of technologies as constraints evolve, and they help the system make better use of the renewables it already has.

AR8 is the window to get this right

Contracts must evolve to reward not just how much generation we build, but system value – prioritising flexibility-ready designs, strategic locations and co-located solutions that reduce curtailment, ease grid stress, reduce system costs and support local industrial growth.

Because ultimately, energy policy works best when it targets real system needs rather than applying one‑size‑fits‑all mechanisms. The same principle applies here: we cannot keep scaling offshore wind through blind, location‑neutral auctions and hope the grid will catch up.

Co-location is not a technology choice – it’s a system design decision. And if the July 2026 AR8 evolves to reflect that, offshore wind can move from being a volume success story to being a system success story that unlocks Clean Power 2030.

Want to know more?

Find out more about how Energy Systems Catapult can help you and your teams

Get in touch

Want to know more?

Find out more about how Energy Systems Catapult can help you and your teams